In today’s healthcare landscape, managing medical expenses can be overwhelming. With rising costs for medical services, prescription drugs, and even routine care, individuals need strategies to save money and plan for healthcare needs. One of the most effective tools available are Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). Both of these accounts offer tax advantages that allow individuals to save money specifically for medical expenses, helping to alleviate some of the financial burdens associated with healthcare. However, while both HSAs and FSAs serve similar purposes, they differ in key ways that can influence which one might be the best choice for your financial situation.

In this article, we will dive into the specifics of each account, the role they play in managing healthcare costs, their benefits, and how to decide which one is right for you.

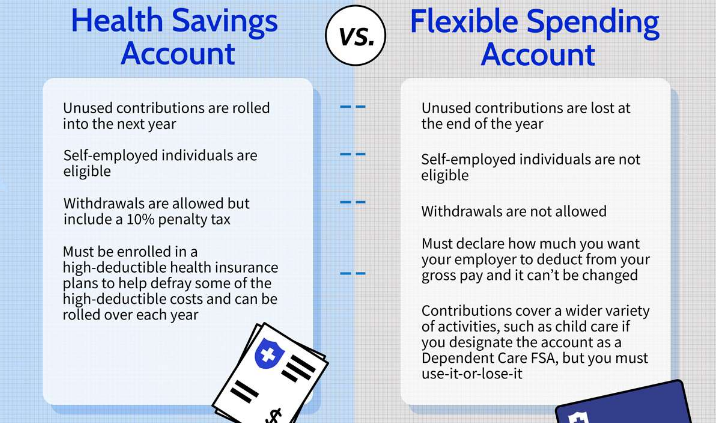

What is a Health Savings Account (HSA)?

A Health Savings Account (HSA) is a tax-advantaged account that allows individuals to save money for medical expenses. To be eligible for an HSA, you must have a high-deductible health plan (HDHP). These plans feature lower premiums and higher deductibles than traditional health insurance, and they are specifically designed to work in conjunction with HSAs.

Key Features of an HSA:

- Tax Advantages: Contributions to an HSA are tax-deductible, meaning they reduce your taxable income for the year. Additionally, the funds in the account grow tax-free, and withdrawals for qualified medical expenses are also tax-free. This triple tax advantage makes the HSA one of the most powerful savings tools available.

- Rollover Funds: Unlike FSAs, the funds in an HSA roll over from year to year. There is no “use it or lose it” rule, so any funds you don’t use in a given year will accumulate and can be used in future years. This makes HSAs an effective long-term savings tool for healthcare costs.

- Portability: HSAs are not tied to an employer. If you change jobs or retire, you can take your HSA with you. This makes it a more flexible option, as the funds are not lost if you move between jobs.

- Contribution Limits: The contribution limits for an HSA are set by the IRS and vary based on your age and whether you are covering just yourself or a family. As of 2025, individuals can contribute up to $3,850, and families can contribute up to $7,750. Those over 55 can contribute an additional $1,000 as a “catch-up” contribution.

- Qualified Medical Expenses: Funds in an HSA can be used for a wide range of qualified medical expenses, including doctor visits, hospital stays, prescription medications, dental care, vision care, and more. Additionally, after age 65, you can use the funds for non-medical expenses without facing a penalty, though you would be subject to ordinary income tax on those withdrawals.

What is a Flexible Spending Account (FSA)?

A Flexible Spending Account (FSA) is another type of tax-advantaged account that helps individuals save for healthcare expenses. FSAs are typically offered through an employer and allow employees to contribute pre-tax dollars to cover medical expenses.

Key Features of an FSA:

- Tax Advantages: Similar to HSAs, contributions to an FSA are made with pre-tax dollars, reducing your taxable income for the year. Additionally, withdrawals used for qualified medical expenses are tax-free.

- “Use It or Lose It” Rule: One of the most significant differences between an FSA and an HSA is that FSA funds generally do not roll over from year to year. If you do not use the funds in your FSA by the end of the plan year (or a grace period, if offered), you will lose them. However, some employers may allow you to carry over up to $500 into the next year or extend the spending period for a limited time.

- Employer-Dependent: Unlike HSAs, FSAs are typically employer-sponsored. This means if you leave your job, you lose access to the FSA. Some plans allow you to continue the FSA through COBRA for a limited time, but for the most part, FSAs are tied to your employment.

- Contribution Limits: In 2025, the maximum contribution limit for an FSA is $3,050, though this limit may vary depending on your employer. As with HSAs, contributions to an FSA are deducted from your paycheck on a pre-tax basis.

- Qualified Medical Expenses: Like HSAs, FSAs can be used for a wide variety of qualified medical expenses. These include doctor visits, prescription drugs, dental and vision care, and over-the-counter medications with a doctor’s prescription.

Comparison: HSA vs. FSA

While both HSAs and FSAs offer tax advantages for healthcare expenses, there are some key differences between the two that may influence which one is best suited to your needs.

- Eligibility Requirements:

- HSA: You must have a high-deductible health plan (HDHP) to open an HSA. This plan often has lower premiums but higher deductibles and out-of-pocket costs.

- FSA: FSAs are offered through employers and don’t have any specific health insurance plan requirements. You can open an FSA regardless of your insurance type.

- Contribution Limits:

- HSA: Contribution limits for an HSA are typically higher than those for an FSA, and they are subject to annual adjustments by the IRS. The limits for 2025 are $3,850 for individuals and $7,750 for families, with an additional $1,000 “catch-up” contribution available for those over 55.

- FSA: FSAs have lower contribution limits. For 2025, the limit is $3,050, which is substantially lower than the HSA’s limits.

- Portability:

- HSA: The funds in an HSA are yours to keep even if you change jobs or insurance plans. This makes an HSA a portable option for long-term savings.

- FSA: FSAs are tied to your employer, meaning you lose access to the account if you leave your job (unless you elect COBRA continuation coverage).

- Rollover Options:

- HSA: One of the biggest advantages of an HSA is that the funds roll over year after year. There’s no need to worry about losing unused funds, and you can accumulate savings for future healthcare needs, especially as you approach retirement.

- FSA: FSAs are subject to the “use it or lose it” rule, which means you must use the funds within the plan year (or any grace period allowed). Some employers may allow a carryover of up to $500, but the bulk of funds in an FSA must be used in the year they are contributed.

- Investment Opportunities:

- HSA: Many HSAs offer the option to invest the funds in stocks, bonds, or mutual funds once your balance reaches a certain threshold. This makes HSAs a powerful long-term savings vehicle for healthcare, especially if you start contributing early.

- FSA: FSAs do not offer investment options. They are designed for short-term use, and any funds you do not use within the plan year are forfeited.

How Can HSAs and FSAs Help with Healthcare Costs?

Both HSAs and FSAs are powerful tools for managing healthcare expenses. Here’s how each account can play a role:

- Managing High-Deductible Plans: If you have a high-deductible health plan (HDHP), an HSA can be a great way to offset the high deductible by saving money tax-free. You can use the HSA funds to pay for out-of-pocket medical expenses like doctor visits, prescriptions, and diagnostic tests.

- Covering Routine and Unexpected Expenses: FSAs are ideal for covering more immediate medical costs, such as copays, over-the-counter medications, dental and vision care, and other routine expenses. The pre-tax contributions help reduce your taxable income, allowing you to save money on taxes.

- Retirement Planning: An HSA can also be a great tool for retirement planning. Once you turn 65, you can withdraw HSA funds for non-medical expenses without facing a penalty (though the withdrawals will be taxed). This makes HSAs a versatile savings vehicle that can double as a retirement account.

Which Is Better: HSA or FSA?

The answer depends on your healthcare needs and financial situation:

- HSA: If you have a high-deductible health plan and want a long-term savings vehicle with flexibility, portability, and investment opportunities, an HSA is a great choice.

- FSA: If you don’t have an HDHP or if you prefer to use the account for shorter-term medical expenses, an FSA may be the better option. FSAs are also beneficial for individuals who want to contribute pre-tax dollars to cover out-of-pocket costs but are comfortable with the “use it or lose it” rule.

Conclusion

Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) are both valuable tools for managing healthcare costs. They provide significant tax advantages and can help reduce the financial burden of medical expenses. Whether you choose an HSA or an FSA depends on your healthcare plan, needs, and long-term goals. By understanding the features and benefits of both accounts, you can make an informed decision that aligns with your financial and healthcare objectives.