Navigating the complexities of healthcare insurance can be overwhelming, especially when it comes to understanding how your claims are processed and what you’re actually responsible for paying. One of the most important documents in this process is the Explanation of Benefits (EOB). Though it’s not a bill, an EOB is essential for understanding how your insurance has processed a claim and what you owe, if anything. This article will explain what an EOB is, why it’s important, and how to read it effectively.

What Is an Explanation of Benefits (EOB)?

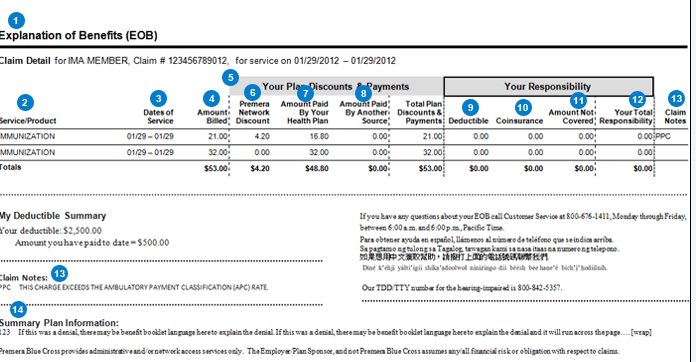

An Explanation of Benefits (EOB) is a statement sent by your health insurance company to explain how a medical claim was processed. It is sent after you receive medical services, such as a doctor’s visit, hospital stay, or medical procedure. The EOB provides a detailed breakdown of the following:

- What the insurer paid: It shows how much the insurance company covered for the specific medical services.

- What you owe: It outlines the amount that you, the insured, are responsible for paying out-of-pocket, if applicable.

- What was not covered: If any part of your claim was denied or excluded, the EOB will explain why.

Despite the name, an EOB is not a bill. Instead, it’s a document that clarifies how your health insurance benefits were applied to a claim. If you owe any amount, you will receive a separate bill directly from your healthcare provider.

Why Is an EOB Important?

An EOB is an essential document for several reasons:

- Transparency: It provides a clear breakdown of how your insurer processed a claim, ensuring transparency in the claims process.

- Verification: The EOB allows you to verify that the charges from your healthcare provider were processed correctly and in accordance with your insurance plan.

- Payment Tracking: It helps you track what the insurance company has already paid, what portion of the claim is covered under your policy, and what you owe.

- Dispute Resolution: If there’s an error or something you don’t understand, the EOB gives you the information you need to contact either your healthcare provider or insurer to resolve any discrepancies.

Understanding how to read your EOB is crucial for managing your healthcare costs and preventing unexpected charges. Below, we’ll walk through the various sections of an EOB to help you understand what each part means.

How to Read an Explanation of Benefits (EOB)

The layout and terminology used in EOBs can vary between insurance companies, but most EOBs contain the same basic elements. Here’s a step-by-step guide on how to read the typical components of an EOB.

1. Patient and Insurance Information

The first section of the EOB typically includes your personal information, including:

- Patient Name: The name of the person who received the medical service.

- Insurance Plan Information: The type of insurance plan under which the claim was processed.

- Policy Number: Your health insurance policy or identification number.

- Claim Number: A unique number associated with the specific claim. This is useful for tracking or disputing a claim.

This section also includes details about your insurance company, such as its contact information, which is helpful if you need to reach them with questions or concerns.

2. Summary of the Claim

In this section, you’ll find an overview of the claim, including the:

- Provider Information: The name of the healthcare provider or facility that rendered the services.

- Service Dates: The dates when the medical services were provided.

- Description of Services: A brief description of the medical services rendered (e.g., doctor’s visit, blood tests, surgery).

- Total Billed Amount: The total amount your healthcare provider has charged for the services.

This section gives you a quick glance at the services that were rendered and the total costs associated with them. It is important to compare the billed amount to what was actually paid to verify that everything is in order.

3. Benefits Applied

This section provides a breakdown of how your insurance policy was applied to the claim:

- Allowed Amount: This is the maximum amount your insurer agrees to pay for the services. If the healthcare provider billed more than the allowed amount, you may be responsible for the difference.

- Covered Amount: This is the portion of the service that is covered by your insurance policy, based on the allowed amount and any applicable copayments, coinsurance, or deductibles.

- Discounts or Adjustments: If your insurance plan has a contract with the healthcare provider, this section will reflect any discounts negotiated by your insurer.

For example, if the total bill for a service was $500 but your insurer has negotiated a lower allowed amount of $400, this section will reflect that discount.

4. What the Insurer Paid

This is one of the most important sections of the EOB because it shows you how much the insurer has paid for the claim. It will show:

- Amount Paid by the Insurer: This is the amount your insurer paid directly to the healthcare provider. This figure will be based on the services covered under your plan.

- Co-payment or Coinsurance: This is the portion of the cost you are required to pay, depending on your insurance plan. For example, if you have a 20% coinsurance rate, you’ll be responsible for 20% of the covered amount, and your insurer will pay the remaining 80%.

For instance, if your insurer paid $350 of a $500 bill and you are responsible for a $50 copay, your total amount owed will be $150 ($50 copay + $100 coinsurance).

5. What You Owe (Patient Responsibility)

The “What You Owe” section shows the amount you are responsible for paying after the insurer has processed the claim. This can include:

- Deductible: If you haven’t met your deductible for the year, you may need to pay a portion of the costs until it’s met.

- Co-pays and Coinsurance: These are the fixed amounts or percentages you pay out-of-pocket for medical services.

- Non-Covered Services: If your insurance plan didn’t cover certain services, those charges will be listed here. Sometimes, this can occur if the service wasn’t deemed medically necessary or if the provider isn’t in your insurer’s network.

It’s important to check this section carefully to ensure the amounts match your policy terms and to spot any errors. If there’s something you don’t understand or disagree with, contact your insurer for clarification.

6. Appeal Process and Additional Information

At the end of the EOB, you may find details on how to appeal the claim if you disagree with the insurance company’s decision. This may include instructions for filing an appeal, deadlines, and any necessary forms.

Additionally, some EOBs may provide details about how you can contact the insurance company if you have questions, or if you need to follow up on unpaid claims.

Common EOB Terms You Should Know

- Copayment (Copay): A fixed amount you pay for a covered health service, typically when you receive the service.

- Coinsurance: A percentage of the total cost of a medical service that you must pay after meeting your deductible.

- Out-of-Pocket Maximum: The most you will have to pay for covered services in a plan year. After reaching this amount, the insurance company pays 100% of covered services.

- In-Network vs. Out-of-Network: In-network refers to healthcare providers that have an agreement with your insurance company, while out-of-network refers to providers who don’t. Out-of-network care usually costs more.

Conclusion

Understanding your Explanation of Benefits (EOB) is crucial for managing your healthcare expenses and ensuring that your insurance benefits are applied correctly. The EOB provides a detailed breakdown of the services you received, how much your insurer paid, and what you owe. By reading and reviewing your EOB carefully, you can catch errors, prevent surprise bills, and better understand your financial responsibility.

If you have any questions about your EOB or notice discrepancies, don’t hesitate to reach out to your insurance company or healthcare provider. They can help you resolve issues and clarify any confusion, ensuring that you’re not overpaying for your care.